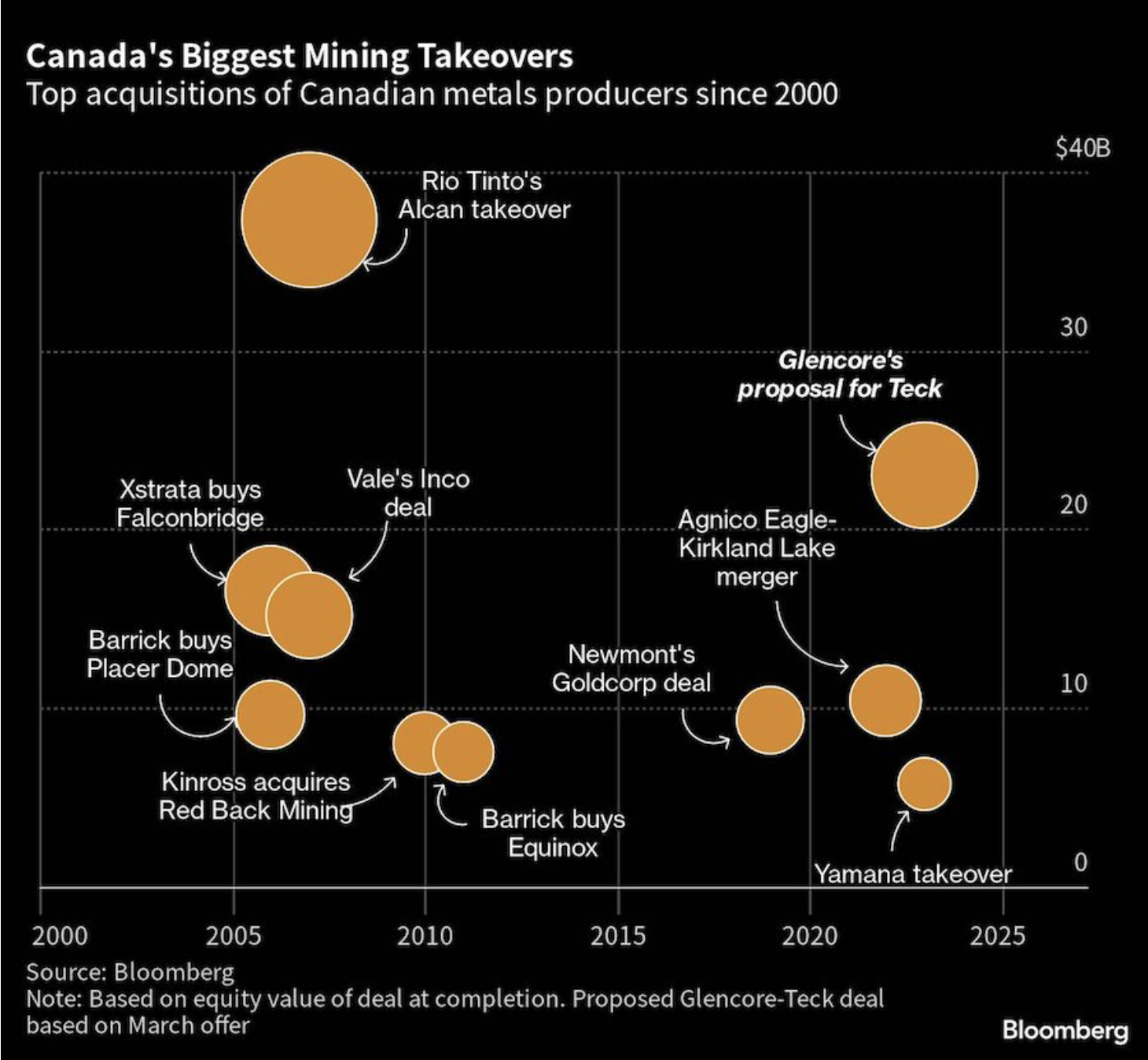

무려 23billion을 주고 Teck을 사려고 했던 글렌코어 인수가 무산될 것으로 보인다. 거의 결정된 것으로 보였던 이 합의가 뒤집어 진 배경에는 Teck의 창업주인 (정확하게 말하면 2세대) Normal Keevil가 있다. 올해 85세인 그는 자신의 기업에 대한 애착이 누구보다 큰 것으로 보이며, 특히 지난 몇 십년동안 유럽이나 미국, 남미 기업에 캐나다 광산 회사들이 팔리는 것을 보면서 꽤나 못마땅했던 것 같다. 아래 기사를 보면 그가 왜 이 회사 집착하는 지에 대한 얘기가 흥미롭게 나와 있다. 캐나다는 산업재 회사가 많기로 유명하다. 아마 호주 다음으로 산업 광물 회사가 많을 것이다 (정확한 건 아님). 그러나 흥미롭게도 캐나다 회사 중에 대형 산업광물 회사는 없다. Teck이 가장 큰 캐나다 회사이고 (현재 20 billon 전후), 이 뒤를 잇고 있는 게 리튬아메라카스인데 규모 차이가 거의 7배 가까이 난다. 그러나 Teck이 큰 다 한들, BHP, Rio, Vale에는 비할바 못 된다. 이 셋은 100조 이상 되는 기업들이다 (주가에 따라 왔다갔다 하긴 하지만).

Teck은 과연 팔릴 것인가. 궁금하긴 하다. 만약 Teck이 팔린다면 LAC도 몇 년 후에 팔라지 말라는 법 없다. 벌써부터 트위터에선 사람들이 일론 보고 돈도 남고 리튬 회사 가격도 떨어졌는데 알버말이 사지 그러냐라는 말이 나오는 판이다.

Teck mining magnate stands between Glencore and mega-deal - MINING.COM

Glencore’s interest doesn’t guarantee a deal gets done. The Keevil family’s control of Teck through voting shares has long insulated the company from takeovers. While Canadian metals producers like Falconbridge Ltd., Inco Ltd. and Alcan Inc. fell to foreign firms in the early 2000s, the family’s iron grip kept Teck independent. Even now, Keevil shows little interest in selling the company he spent decades building.

“He’s like the last of a generation of mine builders in Canada,” said Pierre Gratton, president of the Mining Association of Canada. “You think of all those people that built Canada’s biggest mining companies, and Norm is the last one standing.”

Keevil was born in Cambridge, Massachusetts in 1938 and spent the better part of his childhood in northern Ontario’s wilderness. His father, a Harvard University graduate turned prospector, abandoned academia in the 1950s to develop a small copper deposit near a remote settlement named Teck Township, about 600 kilometers (375 miles) north of Toronto.

‘Rest on your ores’

The mine became a family business, and Keevil joined his father’s company after completing a doctorate in geology from the University of California, Berkeley in the early 1960s. In a 2017 memoir, Never Rest on Your Ores: Building a Mining Company, One Stone at a Time, Keevil recalled attending monthly board meetings in a log cabin on an island across from the mine.

“Norm and his dad really started the company from grassroots, with nothing,” said Edward Thompson, 87, who befriended Keevil in college and became one of Teck’s first executives.

Keevil shared his father’s penchant for high-stakes business gambles, and when Keevil took over as chief executive officer in 1982 he enacted a flurry of acquisitions that netted the company some of its most lucrative base metal operations. At the apex of the 1980s oil shock, he borrowed heavily to finance oil and coal projects in Canada’s western provinces. Later, he sought backing from Japanese and Chinese investors to pitch in on expensive mining ventures further north.

Keevil didn’t possess the typical bravado of mining executives of the time, Thompson said, calling him “aggressive in business, but quite soft-spoken — almost shy.”

“When we’re together, I sometimes have trouble hearing him because he’ll talk so quietly,” he said.

Still, Keevil rarely minced words when it came to business. During the battle to acquire Inco in 2006 — which drew bids from foreign firms as well as Teck — Keevil said its CEO “sold Canada out for his own purposes.”

Today, Keevil lives in British Columbia and has largely retreated from public life. He holds a spot in the Canadian Mining Hall of Fame and has departments named after him at the University of Toronto and University of British Columbia. Keevil didn’t respond to Bloomberg requests for comment.

After Glencore’s proposal, Keevil — who holds an honorary position as chairman emeritus at Teck — issued a brief statement on April 3: “I unequivocally support the board’s decision to reject Glencore’s unsolicited offer to acquire Teck. Now is not the time to explore a transaction of this nature.”

Teck has been protected from such takeovers thanks to the Keevil family’s unusual choice in 1969 to separate shares of the company into two classes, with one set carrying more power than the other. Through a holding company called Temagami Mining Co., the family has the majority of class A shares, each entitled to 100 votes, while the public has class B shares, which carry one vote.

“Without the protection of our dual-share structure, Teck would have been swallowed up,” Keevil wrote in his memoir. “We could have been the target of an opportunistic takeover and a longtime Canadian mining champion lost to foreign hands.”

Corporate filings released on April 3 showed that Teck board members began talks with Keevil a year ago to consider collapsing the share structure, citing growing investor unrest. Keevil and the board spent about four months negotiating before arriving at an agreement in January.

That deal, which requires approval from shareholders in an April 26 vote, would give the Keevils six more years of control of a company they’ve so carefully guarded.

“It’s like giving your baby away,” Thompson said. “It’s tough to see something you spent a lifetime creating disappear.”

(Reporting by Jacob Lorinc).